{kind=link}

Introduction

Rising insurance costs are now a common theme in the United States. Post COVID, as used cars got more and more expensive, and as supply chains shut down, customers saw both new and used car values go up significantly. Inflation also took off at the same time and the cost to repair a car rose through the roof. Both of these factors combined to result in increased car insurance prices.

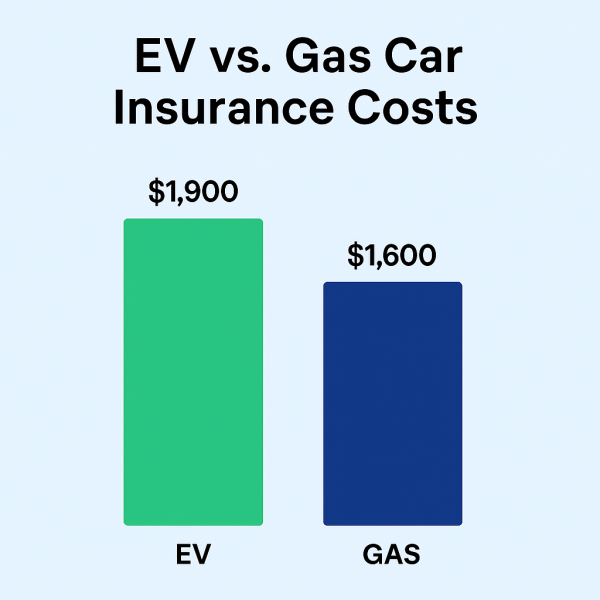

Electric vehicles have also not been immune to these rising insurance costs. In fact, if you compare electric vehicle insurance costs to their ICE counterparts there is a 10 – 25% premium that electric vehicle owners are forced to cough up.

| Vehicle | Type | Avg. Annual Insurance | Source |

|---|---|---|---|

| Tesla Model Y | EV | $2,100 | Bankrate (2024) |

| Hyundai Ioniq 5 | EV | $1,796 | NerdWallet (2024) |

| Ford Mustang Mach-E | EV | $1,884 | NerdWallet (2024) |

| Toyota RAV4 | Gas | $1,700 | Bankrate (2024) |

| Honda CR-V | Gas | $1,540 | The Zebra (2024) |

| Toyota Corolla | Gas | $1,520 | The Zebra (2024) |

So what’s going on here? And more importantly, is this a temporary bump, or are higher insurance costs just part of going electric?

Let’s unpack it.

EVs Are Still Expensive

We hinted at this earlier, but one of the biggest drivers of insurance cost increases is the replacement cost of the car you drive.

Even as EVs have taken off and as prices have come down, the average EV still continues to be a little bit more expensive than an ICE car. In December 2024, the average transaction price for new EVs was reported at $55,544, compared to $49,270 for ICE vehicles, reflecting a difference of approximately $6,274.

So a lot of the higher insurance cost is largely due to the fact that EVs, on average, are still slightly more expensive upfront. The EV market for the past five years has seen mostly luxury sedan or SUVs hitting the market targeting early adopters who wouldn’t mind paying a premium for an EV. Most of the historical insurance cost data mainly includes these expensive EVs and does not include cheaper EVs.

This, however, is changing and will continue to change. A lot of cheaper EVs are set to hit the market over the next few months and years. The Hyundai Kona Electric will be released this year and has an MSRP of $33,000 before tax credits. The Kia EV3 which is already being in sold in Europe and in Asia, will be sold in the US market either this year or the next and will have a price comparable to that of the Hyundai Kona Electric.

Tesla is focused on mass producing a more affordable version of its Model 3 and Model Y at similar price points while Rivian is expected to release its midsize R2 and R3 vehicles, both of which are expected to be below $50,000.

All of these EVs will reduce that replacement cost by a lot, which will reduce EV insurance costs by a lot.

EV Repairs Can Be Tricky

People often assume (wrongly) that EVs are packed with sensors, cameras, and ADAS systems all of which make it more costly to repair. That’s true. But the same is true of most modern ICE cars as well. They too are packed with sophisticated devices and components which are expensive.

So if that’s not true, why are EV repairs slightly more expensive? After all, the chances are that an EV will have a much lower frequency of repairs but when they do need a repair they could be expensive if its out of warranty. A recent report from CCC Intelligent Solutions found that EV repairs cost 25% more on average than repairs for internal combustion vehicles.

There are two reasons.

Not Enough EV Technicians

There are very few auto repair shops that have the know how to fix EVs. Gas cars have been around for more than a 100 years and benefit from thousands of auto shops and maintenance technicians who know how to fix or replace a combustion engine. It will take time for these technicians to learn the craft of repairing EVs.

Gigacasting Is a Double Edged Sword

Companies like Tesla and Rivian use a manufacturing technique called gigacasting, which molds large sections of the car’s frame like the rear underbody into a single aluminum piece. While this makes production faster and cheaper, it creates major challenges for collision repair.

If one part of the casting is damaged, the entire section often needs to be replaced, which can involve disassembling the battery and drivetrain. This makes repairs more complex and costly, and insurers are more likely to declare EVs like the Model 3 a total loss even after moderate accidents.

But not all EV companies are going to be like Tesla or Rivian. We have written a lot about the Bezos backed Slate EV which has largely eschewed the gigacasting model in favor of more modularity. A more modular approach to building EVs should make repairs easier and bring down insurance costs. If Slate gets a lot of traction, expect a lot of companies to replicate the same approach.

Data is Everything

Another reason EV insurance is high especially for newer models is that insurance companies just don’t have that much data yet.

Insurance companies are known to be extremely risk averse and conservative. This means that insurance pricing is to a large extent driven by the availability of actual data on costs and repairs. The more data there is, the better. The less the data there is, the more expensive your premium is going to be.

Insurance companies are extremely comfortable pricing gas cars. They have a well established playbook they can use for cheap and expensive cars. But a Tesla Cybertruck or a Chevy Blazer EV? That’s a new frontier. Without years of claims data, insurers play it safe and often set premiums on the high side to cover unknown risks.

Over time, as more EVs hit the road and insurance companies get better at predicting repair costs, these premiums should come down. That’s not all, as EVs get more and more autonomous, insurers will start to give them credit for being a lot more safer than cars. All of these factors will eventually bring down insurance costs.

The Good News: It’s Getting Better

This isn’t all doom and gloom. In fact, the insurance gap is already starting to shrink. We think that EVs will in the future have a lower insurance cost than traditional gas cars. As adoption continues to increase, cars get cheaper, and more and more body shops get EV training, insurance costs will only decrease in cost.

More insurers are also building out specialized EV coverage. Some, like State Farm and Progressive, even offer discounts for EV owners especially if you use telematics or bundle your policies. They do this because if insurers penalize EV owners with high premiums for too long, new insurance startups that offer a better product for EVs will pop up and take away market share from existing insurance companies.

And when you zoom out, the total cost of owning an EV is still lower for many drivers. You save on gas, oil changes, and maintenance. Even if you’re paying a bit more for insurance now, the long-term economics will still work out in your favor.